I’m not financially literate.

I don’t know the language of “money.”

Can’t understand it and damn sure don’t speak it.

Last time I created a budget, it was an assignment in preparation for graduation. Years ago.

Recently, I realized I have a hard time saying “no” to instant gratification. Unfortunately, that’s a reckless, if not dangerous, way to live. I love to give, and I have a bad habit of sharing until I have nothing left. Largely because I’m not cognizant of how much the little things add up. Therefore, I’m committing to plan and track my spending. *gulp*

Wake Up Call

About month ago, I totaled my car. Prior to that, I’d already committed to make changes to my lifestyle habits. I was actually en route to the gym, when I killed my baby. RIP Micky the Mazda.

“My” car wasn’t in my name. Neither was insurance. Thus, my payments were.. comfortable. That’s all about to change.

I’ll be purchasing my first car and getting my own insurance policy. I’d hoped to transition when I turned 25, since I was told insurance rates would be lower. Consequently, I wasn’t keeping track of my debt, and was turning a blind eye to my credit score. I had to grow up in the course of a couple days, to get a grip on my money matters.

I don’t have any negative activity on my credit now *knocks on wood* …many phone calls and payments later. However, the damage is done. All the old red flags on my report are still flying high. I’ve decided to get a “Bank of America secured credit card” to help reshape my financial reputation. Supposedly, I won’t see much improvement until I’ve had it for a year, but I gotta start somewhere. I hear that putting the car I’m set to buy in my name, will also help (re)build my credit, too. Apparently, I can even refinance the FAT car note I’ll undoubtedly be slapped with, once my score begins to improve.

The Rebel

in me wants to say “f*ck this shit!” Our “paper” (dollar) is a joke. Where’s the gold at?! Who the hell runs the Federal Reserve?! Then the fantasies of living on a mountain, with my own garden for survival, become more appealing. However, I’m not a clean eater (yet!) so I’m going to stay put and play the “credit” game, instead of letting it play me!

Plan of Action

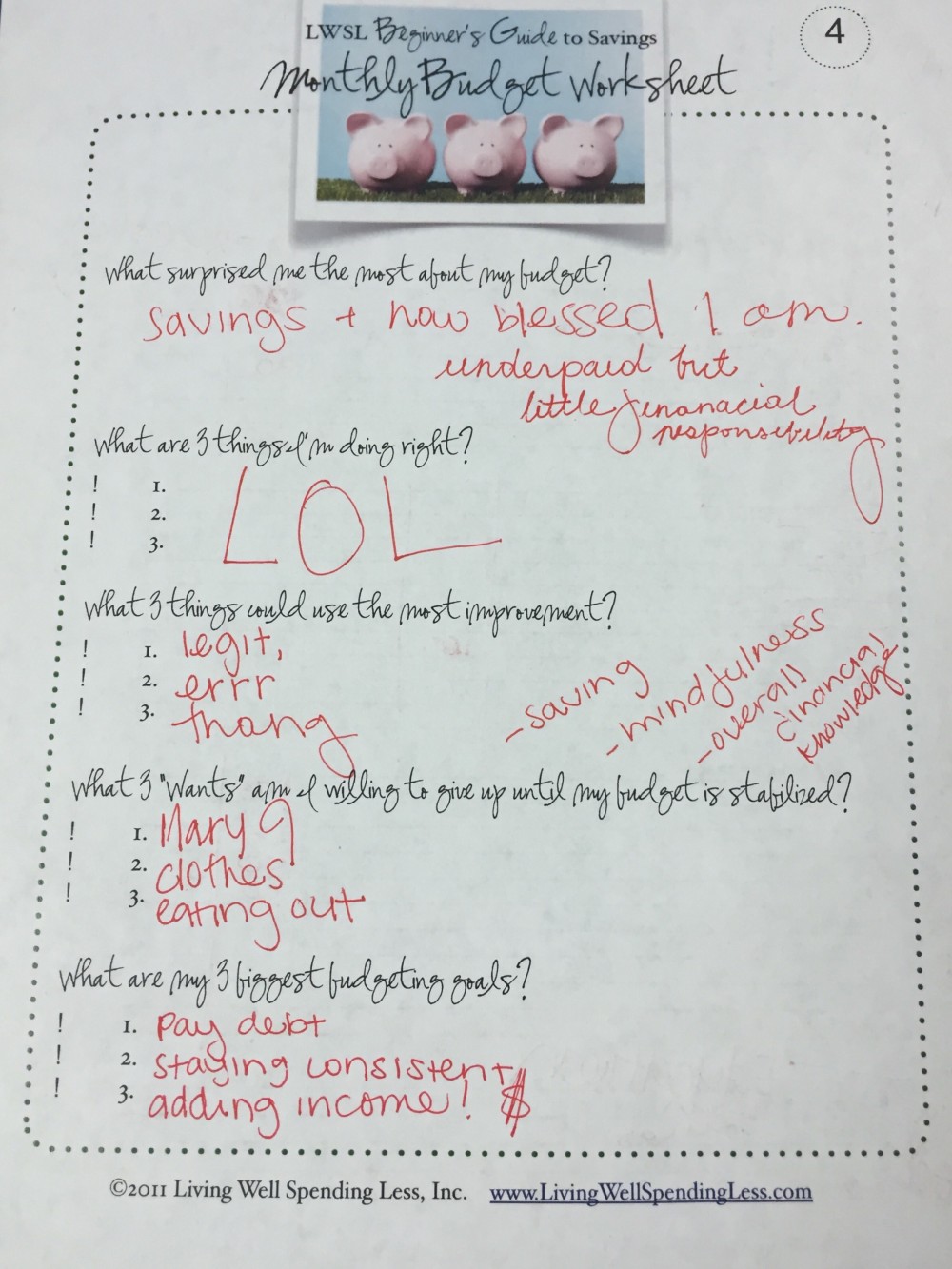

Right before leaving work yesterday, I stumbled upon a printable on pinterest from the Living Well, Spending Less blog. It was a great foundation to get my cogs turning. I was reminded that some of the things I view as “fixed expenses” — aren’t. I also had an epiphany about “saving.” This concept has always alluded me, but I’m going to at least try. Having my savings and checking accounts joined is a FAIL so I’m thinking about kickin’ it old school with a ceramic piggy back. Perhaps I’ll stuff money in a Hennessy bottle.

Since order and simplicity aren’t attributes that describe my thinking patterns, neat surroundings and organized presentations help me feel balanced. I’m going to use the template I scribbled on yesterday to develop my own budget template. I want to customize things down to the typeface, so I have an attachment to it… and use it!

One of my friends Jay, swears by her excel spreadsheet to keep her finances in order. She also keeps paper files. Another on of my BBFs, Janice, raves about mint. Since I’m a newbie to this discipline, I’m going to start by hand. Just like math. I’ll learn the classic formula before using shortcuts!

If you have tips & tricks about how to become more for financially savvy, or resources to share….. leave me a comment!

Great article